The $40,000 SALT Deduction: Who Actually Benefits and How Much They’ll Save

Save Up to $10,500 per year — or $52,500 over five years — if you qualify

The One Big Beautiful Bill Act just quadrupled the state and local tax (SALT) deduction from $10,000 to $40,000 for 2025-2029. Here’s who wins, who loses, and how to calculate your actual savings.

If you want to see your exact savings, I built a simple SALT deduction calculator you can run with your own numbers (linked at the end)

The Quick Summary

What Changed:

SALT deduction cap: $10,000 → $40,000 (2025-2029)

Phaseout: Begins at $500K MAGI, complete at $600K

Must itemize to benefit (standard deduction: $31,500 married / $15,750 single)

Reverts to $10,000 in 2030

Critical Detail: SALT is just ONE component of itemized deductions. You deduct up to $40,000 in SALT (state tax + property tax) PLUS mortgage interest PLUS charitable donations. These stack together.

The Big Picture

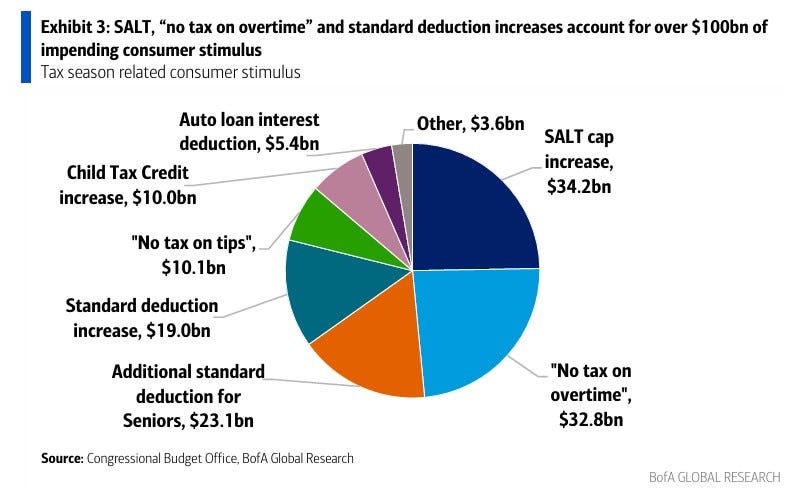

The SALT cap increase represents $34.2 billion in stimulus - the largest single component of the OBBB tax package. For tech employees in California, New York, and New Jersey, this is the most significant tax change affecting your 2025 return.

Source: BofA Global Research, Congressional Budget Office

Who Benefits: The Three Tiers

Tier 1: Maximum Beneficiaries ($8K-$12K annual savings)

Income: $250K-$500K MAGI

High-tax state (CA, NY, NJ, CT, IL, MA)

Homeowner with mortgage

Singles have an edge: Full $40K cap vs. only $15,750 standard deduction makes itemizing a slam dunk

Why they dominate: State taxes + property taxes hit the $40K cap, then mortgage interest and charitable donations stack on top, creating $60K-$80K in total itemized deductions. For singles, the gap over the $15,750 standard deduction is massive.

Tier 2: Moderate Beneficiaries ($3K-$7K annual savings)

High-tax state renters with $300K+ income

Homeowners with paid-off mortgages

The challenge: Without mortgage interest, harder to exceed the $31,500 standard deduction threshold significantly.

Tier 3: Zero Benefit

Three groups get nothing:

Income >$600K (phased out)

No/low-tax states (TX, FL, NV) without expensive homes

Income <$150K or renters (standard deduction better)

The Math: California Example

Profile: Single, $400K income, Bay Area homeowner

Itemized Deductions:

CA state tax: $32,000

Property tax: $18,000

Total SALT: $50,000 → Capped at $40,000

PLUS (separately deductible):

Mortgage interest: $22,000

Charitable donations: $8,000

Total itemized: $70,000 vs. $15,750 standard deduction

Tax Savings:

Old law SALT: $10,000 → Total itemized: $40,000

New law SALT: $40,000 → Total itemized: $70,000

Additional deduction: $30,000

Tax bracket: 35%

Annual savings: $10,500

Five-year total: $52,500

Singles Get a Massive Advantage

Single filers get the full $40,000 SALT cap while the standard deduction is only $15,750. This creates a huge itemization advantage that married couples don’t enjoy.

Important: Married filing separately doesn’t help - the SALT cap drops to $20,000 per person, eliminating any advantage.

The irony: The Trump administration doubled the child tax credit and created “Trump accounts” to incentivize having children, yet the OBBB structure disincentivizes marriage for high earners in expensive states. Two cohabiting singles each get $40K SALT caps; get married and you share one $40K cap.

Advanced Strategies

1. Property Tax Prepayment (Bunching Strategy) Pay both 2025 AND 2026 property taxes in December 2025 to concentrate deductions into one year. This “bunching” strategy lets you maximize the $40K cap in 2025, then take the standard deduction in 2026.

Example:

Normal approach (itemize both years):

2025: $15K property + $18K state = $33K SALT deduction

2026: $15K property + $18K state = $33K SALT deduction

Two-year total: $66K in deductions

Bunching approach:

2025: Pay both years’ property taxes = $30K property + $18K state = $48K SALT → Deduct $40K (capped)

2026: Only state tax = $18K SALT → Take $31,500 standard deduction instead (better than itemizing $18K)

Two-year total: $71,500 in deductions

Bunching advantage: $5,500 more in deductions over two years ($1,925 tax savings at 35% bracket)

This works only if your 2026 property tax bill is already assessed.

2. MAGI Management Near $500K? Max out 401(k) contributions ($23,500 or $31,000 if 50+) to drop below the phaseout threshold. A couple maxing two 401(k)s reduces MAGI by $47,000.

3. Pass-Through Entity Tax (Business Owners) If you own an S-corp or partnership in a state with PTET election, the business pays state tax as an unlimited business deduction, bypassing the individual SALT cap entirely. This workaround remains available.

My Take

From a policy perspective, this is a regressive tax cut benefiting wealthy homeowners in blue states. The JCT estimates it costs $140 billion over 10 years.

But from an individual planning perspective, if you’re in Tier 1, this is $50K+ in tax savings over five years. That’s real capital you can deploy elsewhere.

The intelligent move: recognize where you fall in the distribution, run your specific numbers, and implement bunching strategies if you’re on the margin. Then build that cash flow into your investment plan.

This isn’t about fairness. It’s about optimizing within the tax code as it exists.

Should You Itemize or Take the Standard Deduction?

Not sure whether the higher SALT cap actually helps you?

I built a calculator that shows — with your numbers — whether itemizing makes sense.

Enter a few basics (income, state tax, property tax)

See your estimated federal tax under both methods

Know exactly which option saves you more — and by how much

The $40,000 SALT window only runs from 2025–2029.

This takes under a minute and removes the guesswork.